장비 ·소재 부문의 자급률을 높이기 위한 투자 절실

최근 한국의 수출 1위 품목인 반도체의 수출이 부진한 가운데 다가오는 5g시대를 맞아 국내 반도체 산업 경쟁력에 대한 전반적인 점검이 필요하다는 지적이다.

3일 한국무역협회 국제무역연구원의 '한국 반도체 산업의 경쟁력, 기회 및 위협요인'에 따르면 2017년과 2018년 각각 57.4%, 29.4%씩 급증했던 반도체 수출은 2018년 말부터 감소세를 기록하고 있다. 지난 2년간 지속된 반도체 슈퍼사이클의 기저효과가 크게 작용하고 있다는 사실을 감안해도 한국 반도체 산업에 대한 점검이 필요하다는 지적이 나오는 이유다.

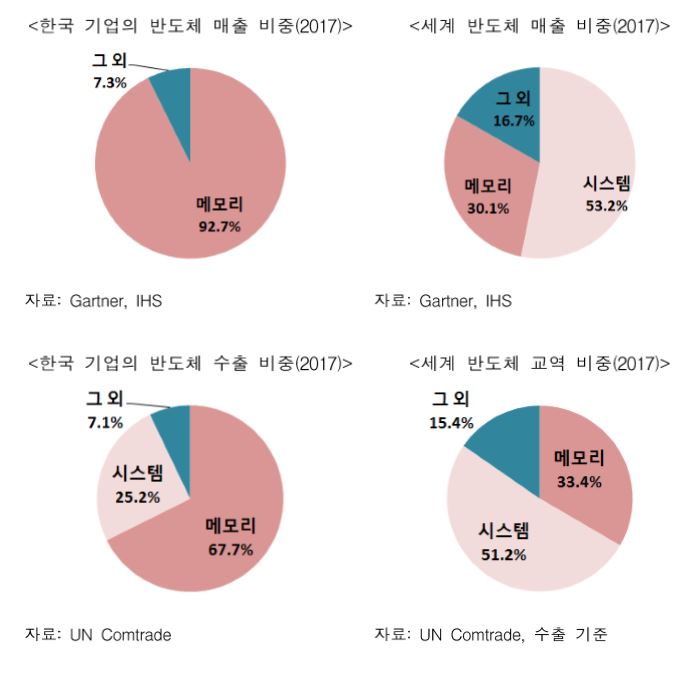

국내 반도체 산업에서 주력 품목으로 자리잡은 메모리는 이미 글로벌 경쟁 우위를 확고히 하고 있다. 2017년 메모리는 전체 한국 반도체 매출의 92.7%, 반도체 수출의 67.7%를 차지했다. 현재 한국의 메모리 산업은 세계 메모리 반도체 시장의 과반을 점유하고 있을 뿐 아니라 기술력도 중국 등 후발국에 비해 월등한 상황이다. 특히 최신 공정 도입을 위해 요구되는 투자규모와 기술력이 크게 증가해 후발기업들의 추격도 쉽지 않은 구조다.

문제는 글로벌 경쟁력이 취약한 시스템 반도체 부문이다. 최근 한국의 파우드리(위탁 제조) 경쟁력은 크게 개선되며 대만에 이어 세계 2위 수준까지 오르는데 성공했지만, 여전히 팹리스 설계 전문 기업 경쟁력은 미국, 일본, 유럽은 고사하고 중국에 비해서도 뒤처지는 모습을 보이고 있다. 세계 반도체 시장 및 교역 규모의 과반은 시스템 반도체가 차지하고 있어 우리나라 반도체 산업이 장기적으로 경쟁력을 유지하기 위해서는 시스템 분야의 경쟁력 강화가 반드시 필요하다는 분석이다.

최근 통신, IT업계의 가장 큰 화두인 5G 서비스, 자율주행차 등 킬러 애플리케이션의 보급 확대는 침체된 반도체 수요가 반등할 수 있는 중요한 기회요인으로 작용할 전망이다. 5G 서비스가 확산됨에 따라 생산되는 데이터의 양은 기하급수적으로 증가해 휴대용 장비 및 데이터센터용 메모리 수요는 필연적으로 증가할 것이기 때문이다.

또한 새로운 서비스를 구현하기 위해 필요한 신개념의 시스템 반도체에 대한 수요는 우리 기업들에게 돌파구가 될 수 있다. 시스템 부문에서는 후발 주자인 한국 기업 입장에서는 자동차용 AP 시장과 같이 누구도 선점하지 못한 시장에서 더 많은 기회를 얻을 수 있을 것으로 보인다.

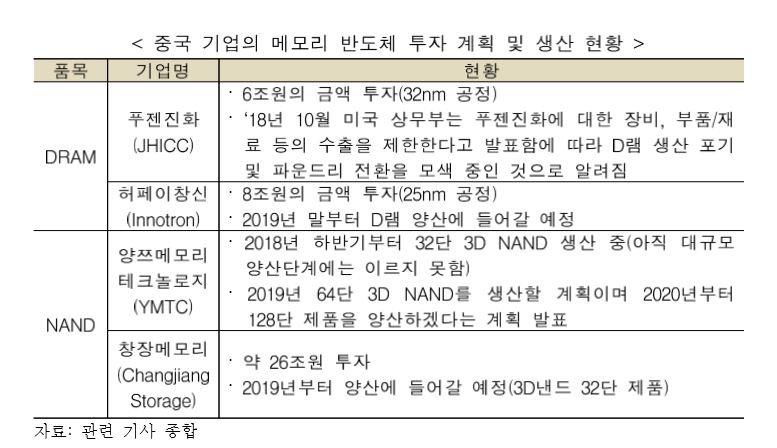

아직 기술적인 격차는 존재하지만 중국 정부의 적극적인 지원 하에 빠르게 성장 중인 중국 반도체 산업은 위협적이다. 메모리 기술력의 차이는 현저하지만 시스템 부문의 기술 격차는 크지 않아 향후 한국의 시스템 반도체 기업과의 경쟁이 심화될 것으로 전망된다. 한국 기업에 대한 중국 정부의 제재와 중국 기업들의 인력 흡수 시도는 이미 진행 중이며 앞으로도 한국 기업들에 부담으로 작용할 것으로 보인다.

미·중 간 반도체 패권 경쟁 구도 또한 두 국가와 모두 밀접하게 연관된 우리 반도체 산업에 리스크로 작용할 전망이다. 미·중 갈등이 지속될 경우 중국의 반도체 공급망은 더욱 더 대만을 중심으로 구성되어 해외공급망에 대한 의존도가 높은 시스템 반도체 산업의 성장에 악영향을 줄 수 있다. 한국이 최대 수출 시장인 중국과 기술 및 장비를 공급받는 미국 사이에 ‘샌드위치’되는 시나리오도 배제할 수 없다.

김건우 한국무역협회 국제무역연구원은 "한국 반도체 산업의 약점을 보완하고 향후 위협요인에 대응하기 위해서는 미 중 분쟁에 따른 피해를 최소화하기 위한 외교적인 노력이 · 필요하다"라며 "또한 해외 반도체 공급망에 대한 의존도를 낮추기 위해서는 국내 반도체 설계 부문을 육성하고 장비 ·소재 부문의 자급률을 높이기 위한 투자가 절실하다."고 말했다.

[Analysis] 5G Era, Korea's semiconductor industry 'Crisis and Opportunity'

Critics point out the need for an overall inspection of the competitiveness of the local chip industry in the upcoming 5G era amid the recent sluggish exports of semiconductors, South Korea's No. 1 export item.

Exports of semiconductors, which surged 57.4 percent and 29.4 percent in 2017 and 2018, respectively, have been on the decline since late 2018, according to the Korea International Trade Association's Institute for International Trade on Thursday. This is why some point out that the inspection of the Korean semiconductor industry is necessary even considering the fact that the base effect of the semiconductor supercycle that has lasted for the past two years is greatly affected.

Memory, which has become a major item in South Korea's semiconductor industry, is already solidifying its global competitive edge. In 2017, memory accounted for 92.7 percent of all South Korean semiconductor sales and 67.7 percent of semiconductor exports. Currently, Korea's memory industry has a dominant share of the global memory chip market, and its technological prowess is superior to that of latecomers such as China. In particular, it is not easy to catch up with late start-ups as the amount of investment and technical skills required to introduce the latest process are greatly increased.

The problem is system semiconductor sector, which is weak in global competitiveness. Although Korea's competitiveness in powder manufacturing has improved significantly recently, it has succeeded in reaching the second-highest level in the world after Taiwan, it still shows that it lags behind China, let alone the U.S., Japan and Europe. As system semiconductors account for a majority of the global semiconductor market and trade volume, it is necessary to strengthen the competitiveness of the system sector in order for Korea's semiconductor industry to remain competitive in the long term.

The recent expansion of the supply of killer applications such as telecommunications, 5G services and self-driving cars, the biggest topic in the IT industry, is expected to serve as an important opportunity for sluggish demand for semiconductors to rebound. As 5G services proliferate, the amount of data produced will increase exponentially, which will inevitably increase the demand for memory for portable equipment and data centers.

Also, the demand for new concept system semiconductors needed to implement new services could be a breakthrough for our companies. From the perspective of Korean companies, which are latecomers in the system sector, more opportunities are expected to be available in markets where no one has taken the lead, such as the automotive AP market.

There is still a technological gap, but the fast-growing Chinese semiconductor industry with active support from the Chinese government is threatening. The gap in memory technology is significant, but the gap in technology in the system sector is not large, which is expected to intensify competition with Korean system semiconductor companies in the future. The Chinese government's sanctions on Korean companies and attempts by Chinese companies to absorb manpower are already underway and are expected to put pressure on Korean companies in the future.

Competition between U.S. and China for semiconductor hegemony is also expected to pose a risk to our semiconductor industry, which is closely related to both countries. If the U.S.-China conflict persists, China's semiconductor supply network will be more centered on Taiwan, which could adversely affect the growth of the system semiconductor industry, which is heavily dependent on foreign supply networks. One cannot rule out the scenario in which South Korea is "sandwich" between China, the largest export market, and the U.S., which receives technology and equipment.

"In order to compensate for the weakness of the Korean semiconductor industry and respond to future threats, diplomatic efforts are needed to minimize the damage caused by conflicts between the U.S. and China," said Kim Gun-woo, an international trade researcher at the Korea International Trade Association. "In addition, investment is needed to foster the domestic semiconductor design sector and increase self-sufficiency of the equipment and materials sector to reduce reliance on overseas semiconductor supply chains."