국내 퇴직 고령자의 극히 일부만 현역시기의 소비수준을 유지할 수 있다는 연구보고서가 나왔다.

KEB하나은행(은행장 지성규)소속의 하나금융경영연구소(소장 정중호)는 국민연금 수급자(65세~74세) 650명에 대한 설문을 실시한 결과, 대부분의 퇴직 고령자가 수입감소로 생활수준이 급격히 하락했으며, 단지 0.6%만이 현역시기의 소비수준을 유지하고 있는 것으로 나타났다고 밝혔다. 아울러 국민연금 수급자의 62%는 국민연금 수급액을 전액 생활비용으로 지출하고 있고, 국민연금 수급자의 현재 노후생활비용도 적정 생활비용인 264만원(가계기준 283만원)에 크게 모자라는 평균 201만원에 불과한 것으로 나타나 노후보장을 위한 국민연금의 역할이 부족한 실정이라고 분석했다.

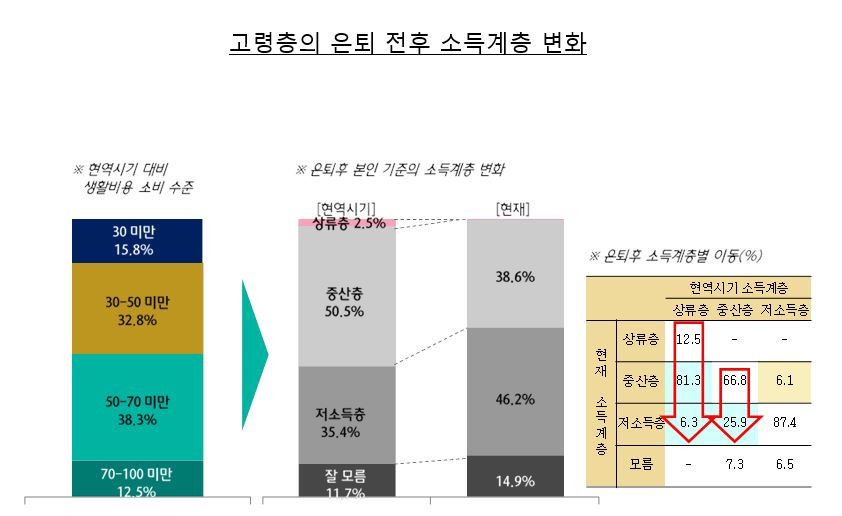

■ 국민연금 수급자의 절반 가까이가 은퇴전 소비수준의 50% 미만에 불과하며, 상류층의 90% 정도는 계층이 하락됐다고 인식

동 설문 분석 결과를 보면, 퇴직 고령자의 생활 소비수준이 은퇴전에 비해 50% 미만 수준이라고 응답한 비중은 절반 가까이에 달하고, 심지어 30% 미만에도 미치지 못한다는 비중도 15.8%에 달하는 등 수급자의 생활수준이 국민연금 수급에도 불구하고 크게 하락한 것으로 분석됐다. 특히 은퇴전 상류층이라고 스스로 인식했던 수급자들이 은퇴후에는 81.3%가 중산층으로, 6.3%는 저소득층으로 전락했다고 응답해 상류층 10명중 9명 정도는 계층이 하락했다고 느끼고 있는 것으로 나타났다.

또 국민연금 수급자의 현재 노후생활비용은 월평균 201만원으로 통계청이 제시한 적정생활비용 수준인264만원에 한참 못 미치고 있으며, 퇴직 후 생활소비 수준이 현역 시기와 비슷한 수준을 유지하고 있는 비중도 0.6%에 불과하다고 응답했다.

■노후준비는 일찍 시작하지만 실제 준비상황은 크게 부족한 실정

절반 이상의 수급자들은 50세 이전부터 노후자금 준비를 시작한 것으로 응답해(20/30대 12.8%, 40대 41.5%) 예상보다는 일찍 노후를 대비해왔으나, 정작 현재의 노후생활비용은 적정 생활비용에 미치지 못하고 있고, 보유 금융자산의 소진 예상 시기도 평균 82세 정도로 나타나 100세 시대의 노후 자금 여력은 많이 부족한 것으로 분석됐다. 향후 추가적인 자금원 마련에 대해서도 수급자의 52.6%는 아예 없다고 응답하거나, 33.8%는 자녀의 부양을 기대한다고 응답해 적극적인 노후대책도 없는 실정이다.

■소득계층별로 희망 금융자산은 뚜렷하게 대비

국민연금 수급자의 61.5%는 지급받은 국민연금을 전액 생활비용으로 지출하고 있으며, 금융상품에 투자하거나 저축하는 비중은 27.1%에 불과하다고 응답했다. 향후 희망하는 금융상품으로는 연금(19.9%)과 건강보험 상품(18%)의 선호도가 높았으며, 소득계층별로는 중산층은 안정적인 노후생활을 위한 추가소득원으로서 연금을 선호한 반면, 저소득층은 비용절감 목적의 건강보험을 가장 선호하는 것으로 나타나 소득수준에 따라 금융상품의 선호도가 뚜렷하게 대비됐다.

■지속적인 소득활동 참가가 중요하며, 금융기관의 맞춤형 금융서비스가 강화될 필요

비재무적 은퇴준비에 대해서는 73.5%가 중요성을 인식하고 있으며, 건강(30.3%)과 나만의 여가(20.3%) 등을 가장 중요한 비재무적 준비활동이라고 응답했다. 그리고 소득활동에 참가하고 있거나 보유자산 규모가 클수록 비재무적 은퇴생활에 대한 만족도도 높아지고 있는 것으로 조사됐다.

김지현 수석연구원은 “현재 42.3%인 수급자의 소득활동 참가율을 최대한 끌어올려 경제력 문제를 해결하는 동시에 자아실현을 통한 감성적 충족을 느끼는 것이 중요”하며, KEB하나은행 연금사업본부 차주필 본부장은 “이번 설문으로 수급자의 소비생활과 노후자금 운용에 대한 실태를 파악하고, 이를 토대로 연령별/소득계층별 맞춤형 금융서비스를 강화할 계획”이라고 밝혔다.

[Analysis] Only 0.6% of retired senior citizens maintain active-duty consumption levels...I'm gonna keep working after I retire.

A research report showed that only a small portion of retired senior citizens in Korea can maintain the level of consumption during the active-duty.

The Hana Financial Management Research Institute (Chairman Jung-ho), affiliated with KEB Hana Bank (Bank President Ji Sung-kyu), said the survey of 650 recipients of the national pension program (65~74 years old) showed that most retired senior citizens saw their living standards fall sharply due to decreased income, and only 0.6 percent of them maintained their consumption levels during the active period. In addition, 62 percent of the recipients of the national pension spend their entire national pension on living expenses, and only 2.1 million won on average, which is far short of the current 2.64 million won (2,830,000 won on household basis), which lacks the role of the national pension fund to run for president.

■ Nearly half of the recipients of the national pension plan are less than 50% of the pre-retirement consumption level, and 90% of the upper class are perceived to have dropped in class.

According to the results of the survey, nearly half of the respondents said that their living standards are less than 50 percent compared to those before retirement, and 15.8 percent said they are less than 30 percent, indicating that the standard of living for the recipients has declined despite the supply and demand of the national pension. In particular, recipients who recognized themselves as "upper class" before retirement said 81.3 percent of them had fallen to the middle class and 6.3 percent to the low-income bracket after retirement, indicating that about nine out of every 10 people in the upper class felt their class had fallen.

In addition, the pensioner said that the current cost of living in old age is 2.10 million won per month, far below the appropriate cost of living, which the NSO suggested, and that only 0.6 percent of the post-retirement living expenses remain at a level similar to when they are active.

■Although age preparation starts early, actual preparation is very insufficient.

More than half of the recipients responded that they started preparing for retirement funds before the age of 50, and had been preparing for retirement earlier than expected (from 12.8 percent in their 30s and 41.5 percent in their 40s), but the current cost of living is not up to the proper cost of living, and the estimated time of depletion of their financial assets is around 82, indicating that they are not able to afford much of retirement funds in the age 100 years. Regarding the future funding of additional funding sources, 52.6 percent of the recipients said they did not have any, or 33.8 percent said they expected to support their children, which means there is no active retirement plan.

■ Clear contrast to desired financial assets by income class

Some 61.5 percent of pensioners said they spend the national pension they received on their entire living expenses, and only 27.1 percent said they invest or save in financial instruments. In the future, the preference for pension (19.9%) and health insurance products (18%) was high, while the middle class preferred pension as an additional source of income for stable retirement, while low-income people preferred health insurance for cost-cutting purposes, which clearly contrasted their preference for financial instruments according to income levels.

■Continuous participation in income activities is important, and customized financial services of financial institutions need to be strengthened

As for non-financial retirement arrangements, 73.5 percent said they recognize the importance, while health (30.3 percent) and leisure (20.3 percent) were the most important non-financial preparatory activities. The survey also found that the greater the size of assets held or income participation in income activities, the more satisfied people are with their non-financial retirement.

"It is important to solve the economic power problem by raising the current 42.3 percent participation rate in income activities to the maximum extent possible, while also feeling emotional satisfaction through self-realization," said senior researcher Kim Ji-hyun. "With this survey, we will strengthen financial services tailored to each age/income bracket based on the survey."